Using blockchain for identity management in KYC for high-end purchases boosts your security and privacy. It lets you verify identities swiftly without needing to share sensitive documents, reducing risks. Your personal data stays encrypted, and you control what gets shared during transactions. With a decentralized verification process, you can trust that your identity is authentic and secure. Discover how blockchain can streamline your luxury shopping experience even further.

Key Takeaways

- Blockchain streamlines KYC processes by enabling quick identity verification, reducing delays in high-end purchase transactions.

- Decentralized verification eliminates reliance on a single authority, enhancing reliability and security for luxury buyers.

- Users maintain control over their digital identities, sharing only essential information during verification to protect personal data.

- Immutable transaction records on blockchain promote transparency, ensuring authenticity and reducing the risk of fraud in high-value purchases.

- Secure digital identities facilitate seamless luxury shopping experiences, minimizing the need to share sensitive documents.

As digital identities become increasingly vulnerable to breaches and fraud, many people are turning to blockchain technology for a more secure solution. When it comes to high-end purchases, you want to guarantee that your identity remains protected while also making the process seamless. By utilizing blockchain for identity management, you can leverage decentralized verification to authenticate your digital identity without compromising your personal information.

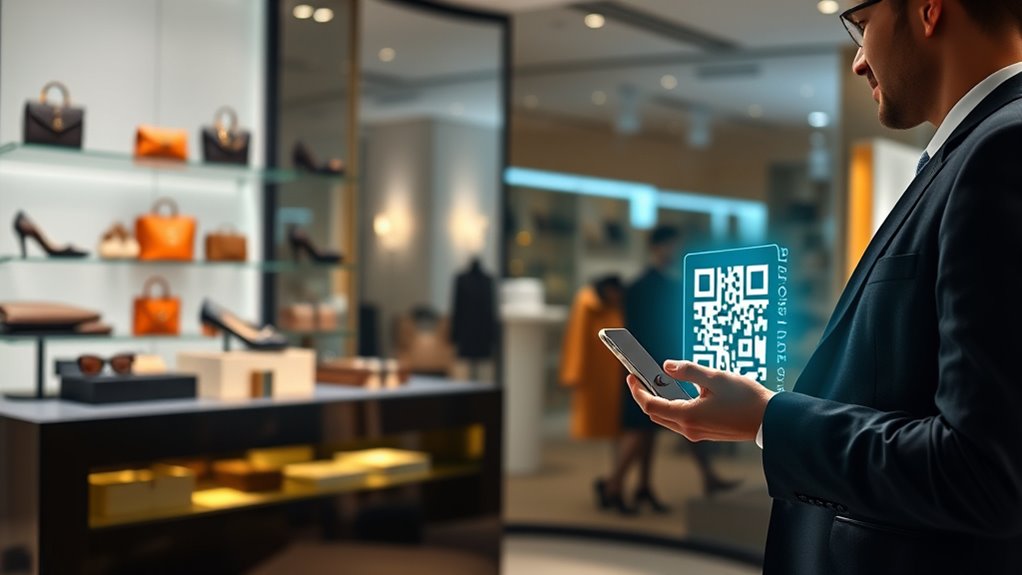

Imagine walking into a luxury store, ready to make a significant purchase. In traditional settings, you might have to share sensitive documents and personal data, which can be risky. However, with blockchain, your digital identity is stored securely on a decentralized ledger, making it nearly impossible for unauthorized access or tampering. This technology allows you to verify your identity in a way that prioritizes security and privacy.

Imagine a luxury shopping experience where your digital identity is securely stored on a blockchain, ensuring privacy and protection.

When you engage in a high-end transaction, decentralized verification plays a vital role. Instead of relying on a single entity to validate your information, multiple nodes across the blockchain network work together to confirm your identity. This means that your data isn’t just stored in one place, reducing the chances of a breach. You can present your digital identity to merchants confidently, knowing that only the necessary information is shared while sensitive details remain encrypted.

Utilizing blockchain for Know Your Customer (KYC) processes simplifies the verification of your identity. Instead of filling out lengthy forms and providing copies of your documents, blockchain allows you to verify your identity in an instant. When a merchant needs to confirm your eligibility for a purchase, they can access your verified digital identity without ever seeing your personal data. You maintain control over what information is shared and with whom, which is increasingly important in today’s digital landscape. Additionally, this method enhances color accuracy in identity verification processes, ensuring that the information presented is both reliable and precise.

Moreover, blockchain technology provides a tamper-proof record of your transactions. Every purchase made can be traced back, ensuring transparency and accountability. This is particularly valuable in high-end markets, where authenticity is paramount. You can showcase your verified digital identity and transaction history, assuring sellers of your legitimacy.

Blockchain for Information Security and Privacy

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Frequently Asked Questions

How Does Blockchain Enhance Privacy in KYC Processes?

Blockchain enhances privacy in KYC processes through cryptographic privacy and data minimization. By using cryptographic techniques, your sensitive information remains secure and only accessible to authorized parties. Data minimization ensures you only share necessary details, reducing exposure to potential breaches. This way, you maintain control over your identity while still complying with regulations. Overall, blockchain creates a more private and secure environment for handling your personal information during KYC procedures.

What Are the Costs Associated With Implementing Blockchain for KYC?

Imagine a luxury car dealership wanting to use blockchain for KYC. The costs can add up quickly. You’ll need to conduct a thorough cost analysis, factoring in software development, infrastructure, and training. Implementation challenges like integration with existing systems can increase expenses, too. While the initial investment may seem steep, the long-term benefits could outweigh the costs, offering enhanced security and efficiency for both you and your clients.

Can Blockchain KYC Systems Be Hacked?

Yes, blockchain KYC systems can be hacked, despite their enhanced security. While the decentralized nature of blockchain makes it harder for attackers to manipulate data, cybersecurity vulnerabilities still exist, like smart contract flaws and human errors. Additionally, regulatory challenges can create gaps in compliance that hackers could exploit. You must remain vigilant and continuously update your security protocols to minimize risks and protect sensitive information in these systems.

How Does User Consent Work in Blockchain KYC?

In a theoretical situation, envision you’re employing a blockchain KYC platform to acquire a premium timepiece. User agreement in this setting signifies you manage your digital profile and approve particular data sharing. When you start a transaction, you give approval for the pertinent entities to confirm your details without revealing it entirely. This approach preserves confidentiality while guaranteeing adherence, making the procedure safe and streamlined for luxury acquisitions.

What Industries Can Benefit Most From Blockchain KYC Solutions?

You’ll find that industries like finance, healthcare, and luxury goods can benefit greatly from blockchain KYC solutions. These sectors rely heavily on secure digital identity verification to guarantee regulatory compliance. By utilizing blockchain, companies can streamline their processes, enhance data security, and improve customer trust. In finance, for example, it can simplify onboarding, while in healthcare, it protects sensitive patient information, making compliance easier and more efficient.

digital identity wallet for luxury shopping

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Conclusion

In a world where trust is as valuable as gold, leveraging blockchain for KYC in high-end purchases can transform identity management. By ensuring secure, transparent transactions, you’re not just protecting yourself; you’re stepping into a future where privacy reigns supreme. Embracing this technology means you’re not just keeping up with the times—you’re riding the wave of innovation, making every purchase not just a transaction, but a leap toward a smarter, safer tomorrow.

KYC blockchain solution for high-end purchases

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Blinq Digital Business Card – NFC Card – Instant Share via Tap – Compatible with iPhone & Android (Black)

FREE FOREVER, NO SUBSCRIPTION — Unlike other NFC business cards that charge monthly fees, Blinq includes unlimited digital…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.